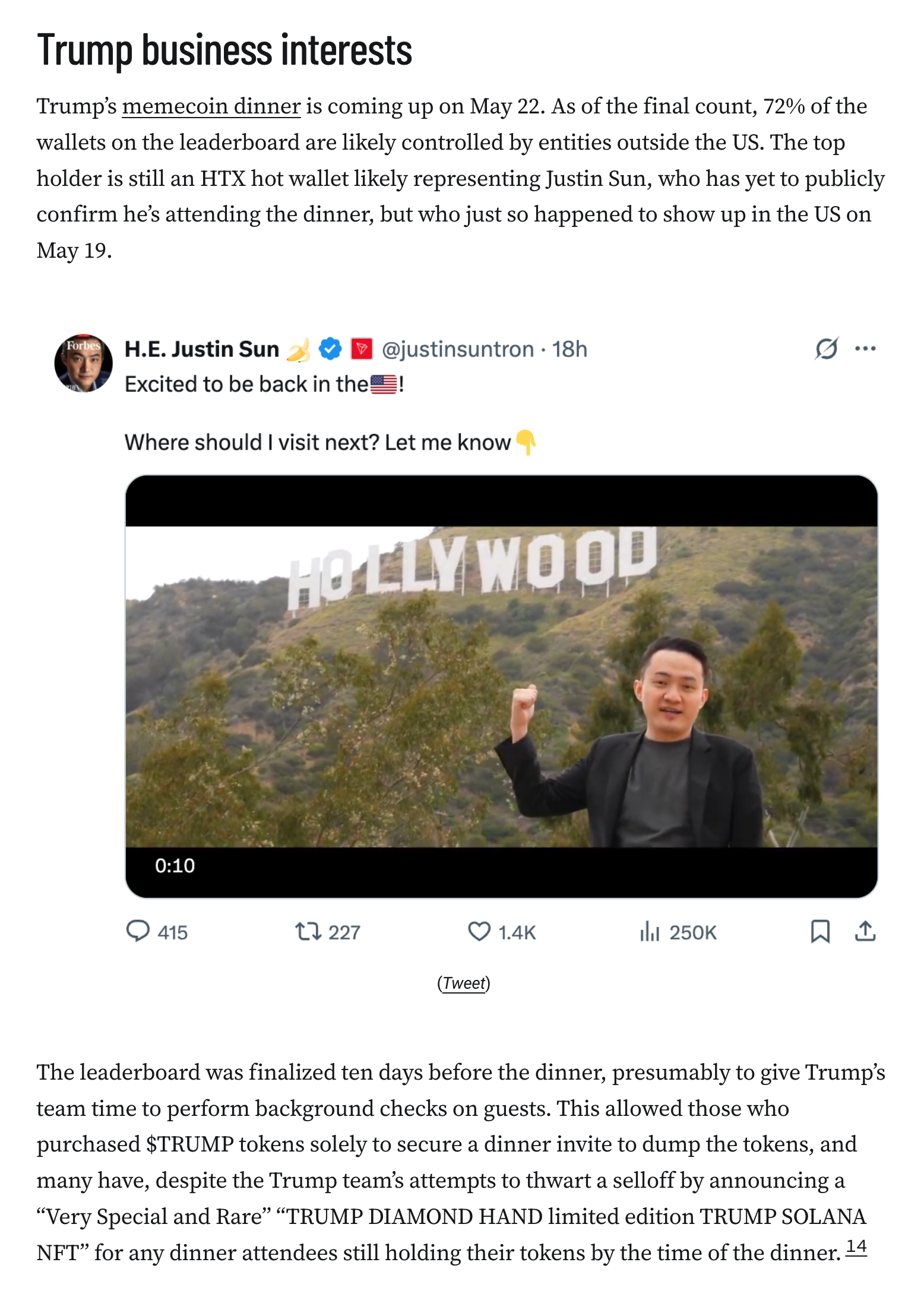

Coinbase has disclosed a substantial customer data breach, blaming it on “rogue overseas support agents”. This follows months of crypto security researchers warning about apparent security issues at the company.

According to Coinbase, the data thieves bribed members of Coinbase’s support team, which is based overseas and reportedly makes very little money. It seems Coinbase has been aware of a breach for several months, but only reported it on May 14.

At least five lawsuits have been filed about the breach in the days since, but a change to Coinbase’s customer agreement that went into effect on May 15 may make it more challenging for customers to obtain relief.

At least five lawsuits have been filed against Coinbase since the breach disclosure.5 However, an incredibly conveniently timed update to Coinbase’s customer terms, announced on April 12 and applying to disputes filed after May 15, may make it more challenging for these cases to succeed. While Coinbase’s customer terms previously contained some text seeking to limit class action lawsuits and force customers into arbitration, the update made some key changes, most significantly aiming to force lawsuits to be filed in New York. The new version also expands clauses limiting collective litigation, mass arbitration, and sharing of information between separate parties involved in arbitration proceedings against Coinbase. It also aims to force any claims that do proceed in court rather than arbitration to go to a bench trial instead of a trial by jury, reduces thresholds triggering batch arbitration, and much more prominently highlights the “Class, Collective, Representative, and Mass Action Waiver and Jury Trial Waiver”.

Of the five lawsuits filed against Coinbase for the data breach thus far, all are class actions, none were filed before May 15, and two were filed outside of New York.

According to Coinbase, the data thieves bribed some members of Coinbase’s poorly paid offshore customer support team, who they described as “rogue overseas support agents”, who are reportedly earning less than $5,000 annually.2 Coinbase’s cybersecurity disclosure filing with the SEC admitted that they had been grappling with this issue for months: “The threat actor appears to have obtained this information by paying multiple contractors or employees working in support roles outside the United States to collect information from internal Coinbase systems to which they had access in order to perform their job responsibilities. These instances of such personnel accessing data without business need were independently detected by the Company’s security monitoring in the previous months.”3 Bloomberg later reported that “the hackers did have near-constant access to some of Coinbase Global Inc.’s most valuable customer data since January”, citing an anonymous source familiar with the incident.4

![Coinbase

On May 12, Coinbase announced it will join the S&P 500 as its “first and only crypto company”.1a This is the latest change that may see more American investors inadvertently exposed to the cryptocurrency industry via index funds, following MicroStrategy’s entry into the NASDAQ-100 in December 2024 [I72].

Their joy was likely tempered when, only two days later on May 14, they had to announce a data breach that exposed customer data including names, addresses, phone numbers, email addresses, images of government ID documents, account balance and transaction data, and masked social security and bank account numbers. Although leaks like this typically lead to an uptick in phishing attempts, where scammers use the private information to contact customers and more convincingly impersonate Coinbase employees, the leak of account balance data and customer addresses is also particularly concerning given the recent spike in violent attacks and kidnappings targeting wealthy crypto holders.

Crypto security researchers have been warning for months about Coinbase’s evidently poor security practices and lack of attention to customer complaints, and describing hacks in which victims reported being scammed by attackers who seemed to have access to private Coinbase data [I76]. In February, zachxbt wrote: “Coinbase needs to urgently make changes as more and more users are being scammed for tens of millions every month. ... Coinbase is in a position where they have the power to make](https://media.hachyderm.io/media_attachments/files/114/542/355/565/850/346/original/ed7d433d8bf281ce.png)

Coinbase

On May 12, Coinbase announced it will join the S&P 500 as its “first and only crypto company”.1a This is the latest change that may see more American investors inadvertently exposed to the cryptocurrency industry via index funds, following MicroStrategy’s entry into the NASDAQ-100 in December 2024 [I72].

Their joy was likely tempered when, only two days later on May 14, they had to announce a data breach that exposed customer data including names, addresses, phone numbers, email addresses, images of government ID documents, account balance and transaction data, and masked social security and bank account numbers. Although leaks like this typically lead to an uptick in phishing attempts, where scammers use the private information to contact customers and more convincingly impersonate Coinbase employees, the leak of account balance data and customer addresses is also particularly concerning given the recent spike in violent attacks and kidnappings targeting wealthy crypto holders.

Crypto security researchers have been warning for months about Coinbase’s evidently poor security practices and lack of attention to customer complaints, and describing hacks in which victims reported being scammed by attackers who seemed to have access to private Coinbase data [I76]. In February, zachxbt wrote: “Coinbase needs to urgently make changes as more and more users are being scammed for tens of millions every month. ... Coinbase is in a position where they have the power to make

![In government

The GENIUS Act stablecoin bill has already advanced in the Senate, after all Democrats and several Republicans voted against it less than two weeks ago amid concerns about Trump’s serious crypto conflicts of interest [I83]. Some Democrats tried to insist that any stablecoin bill include explicit prohibitions preventing the president, Congress members, and others in government from creating and selling digital assets; others, such as the bill’s co-sponsor and longtime crypto industry ally Kirsten Gillibrand, argued that Trump’s crypto activities are “already illegal” and that the bill shouldn’t “deal with all of President Trump’s ethics problems”.20

Despite little in the way of acquiescence to Democrats’ requested changes, 16 Democrats voted in support of the cloture motion: Alsobrooks (MD), Blunt Rochester (DE), Booker (NJ), Cortez Masto (NV), Fetterman (PA), Gallego (AZ), Gillibrand (NY), Hassan (NH), Heinrich (NM), Lujan (NM), Ossoff (GA), Padilla (CA), Rosen (NV), Schiff (CA), Slotkin (MI), Warner (VA).21 The bill will now go to a full vote, likely this week, and will likely still pass after a symbolic but unsuccessful vote on an amendment to limit Trump’s crypto involvement.

The breakneck pace of this bill is likely due to the crypto industry’s concern that their influence on Congress might diminish after the midterm elections. “We have a very narrow window to get legislation through. The midterms are next year. I think it’s very](https://media.hachyderm.io/media_attachments/files/114/542/367/879/336/404/original/d98137ce19666706.png)