Newsletter: The Trumps “debank” major customers from their “anti-debanking” cryptocurrency venture, and a CFTC nominee says the Winklevosses are blackballing him

Discussion

Loading...

Post

@span molly0xfff hello how are!

@molly0xfff um akshully the plural is Winklevi

The Trump family scored huge windfalls this week as WLFI became available for trading, and American Bitcoin went public. Their WLFI stake has been reported at multi-billions of dollars, though this valuation suffers from the usual crypto pricing issues I’ve written about before.

![One could reasonably complain that I’m counting the trees while the forest burns on this point. While I do think it’s important not to present misleading numbers, it’s inarguable that the Trumps have profited enormously from World Liberty. With 75% of WLFI token sale proceeds flowing directly to the Trumps after an initial $30 million threshold was met, the Trumps profited $412.5 million from the early token sales. The token has also served as a mechanism for indirect payments to the president and his family — crypto billionaire Justin Sun’s $75 million purchases of WLFI in November 2024 and January 2025 saw $56 million of it flow directly to the Trumps. Besides that, the family has a massive share of WLFI tokens they will later be allowed to sell (though not for $5 billion) or potentially borrow against. And the family maintains an equity stake in the company, giving them a share of all ongoing operations. One significant revenue stream comes from the USD1 stablecoin — particularly its use by the Emirati firm MGX for an investment into Binance [I83]. This arrangement alone is projected to generate $280 million by the end of Trump’s term, with approximately $168 million of it flowing to the Trump family.2](https://media.hachyderm.io/media_attachments/files/115/192/126/425/950/191/original/6231b762efab639e.png)

One could reasonably complain that I’m counting the trees while the forest burns on this point. While I do think it’s important not to present misleading numbers, it’s inarguable that the Trumps have profited enormously from World Liberty. With 75% of WLFI token sale proceeds flowing directly to the Trumps after an initial $30 million threshold was met, the Trumps profited $412.5 million from the early token sales. The token has also served as a mechanism for indirect payments to the president and his family — crypto billionaire Justin Sun’s $75 million purchases of WLFI in November 2024 and January 2025 saw $56 million of it flow directly to the Trumps. Besides that, the family has a massive share of WLFI tokens they will later be allowed to sell (though not for $5 billion) or potentially borrow against. And the family maintains an equity stake in the company, giving them a share of all ongoing operations. One significant revenue stream comes from the USD1 stablecoin — particularly its use by the Emirati firm MGX for an investment into Binance [I83]. This arrangement alone is projected to generate $280 million by the end of Trump’s term, with approximately $168 million of it flowing to the Trump family.2

![WLFI opens for trading

World Liberty Financial’s WLFI token, previously a non-resalable “governance token” available for purchase only by non-US buyers and accredited US investors, has become available for secondary trading following a July governance vote [I88]. After trading opened, the Wall Street Journal ran the headline: “Trump Family Amasses $5 Billion Fortune After Crypto Launch”.1 In the article’s subtitle and body text, the Journal acknowledges that these are merely “paper” profits, quietly walking back the misleading headline figure. Flawed estimates of dollar-denominated windfalls — which ranged from around $4 to $6 billion depending on outlet — are a recurring issue in crypto reporting, as I discussed in my January article “No, Trump didn’t make $50 billion from his memecoin”. For one, the Trumps and other members of the project team are not yet permitted to actually sell any of their tokens. But even if they were, large sales of tokens in low-liquidity markets inevitably cause token prices to collapse, making the price × quantity equation a poor estimate for the dollar value of large holdings. The Trump family faces even further challenges to cashing out: any significant selling of their stash would likely trigger market panic as investors rush to interpret what the insider sales signal.](https://media.hachyderm.io/media_attachments/files/115/192/126/421/378/537/original/4fcbf138dec94565.png)

WLFI opens for trading

World Liberty Financial’s WLFI token, previously a non-resalable “governance token” available for purchase only by non-US buyers and accredited US investors, has become available for secondary trading following a July governance vote [I88]. After trading opened, the Wall Street Journal ran the headline: “Trump Family Amasses $5 Billion Fortune After Crypto Launch”.1 In the article’s subtitle and body text, the Journal acknowledges that these are merely “paper” profits, quietly walking back the misleading headline figure. Flawed estimates of dollar-denominated windfalls — which ranged from around $4 to $6 billion depending on outlet — are a recurring issue in crypto reporting, as I discussed in my January article “No, Trump didn’t make $50 billion from his memecoin”. For one, the Trumps and other members of the project team are not yet permitted to actually sell any of their tokens. But even if they were, large sales of tokens in low-liquidity markets inevitably cause token prices to collapse, making the price × quantity equation a poor estimate for the dollar value of large holdings. The Trump family faces even further challenges to cashing out: any significant selling of their stash would likely trigger market panic as investors rush to interpret what the insider sales signal.

The World Liberty project, which the Trump sons say they created to fight “debanking”, is getting some flak for freezing holders’ tokens — including those belonging to some of their biggest backers, like billionaire Justin Sun.

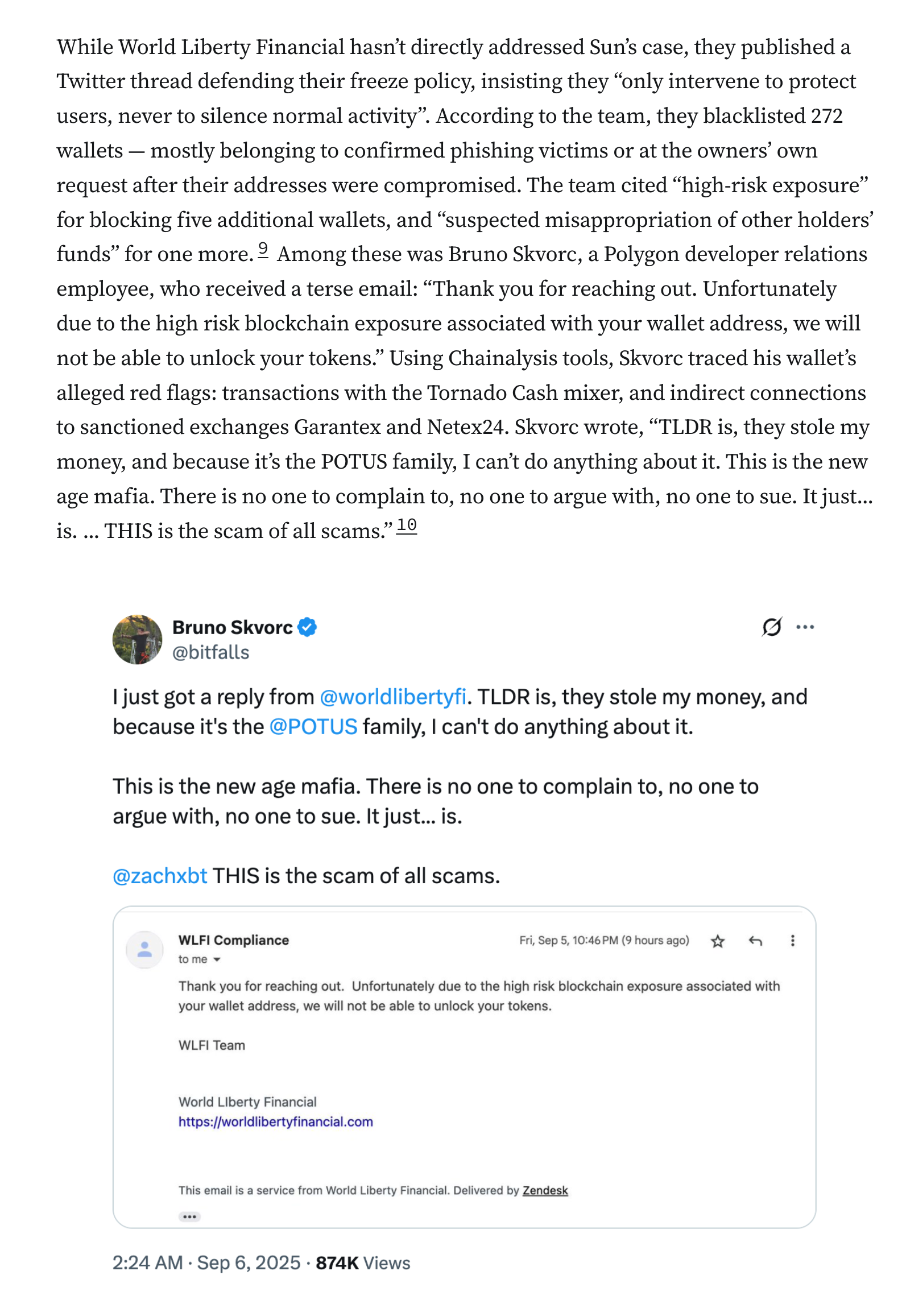

While World Liberty Financial hasn’t directly addressed Sun’s case, they published a Twitter thread defending their freeze policy, insisting they “only intervene to protect users, never to silence normal activity”. According to the team, they blocklisted 272 wallets — mostly belonging to confirmed phishing victims or at the owners’ own request after their addresses were compromised. The team cited “high-risk exposure” for blocking five additional wallets, and “suspected misappropriation of other holders’ funds” for one more.9 Among these was Bruno Skvorc, a Polygon developer relations employee, who received a terse email: “Thank you for reaching out. Unfortunately due to the high risk blockchain exposure associated with your wallet address, we will not be able to unlock your tokens.” Using Chainalysis tools, Skvorc traced his wallet’s alleged red flags: transactions with the Tornado Cash mixer, and indirect connections to sanctioned exchanges Garantex and Netex24. Skvorc wrote, “TLDR is, they stole my money, and because it’s the POTUS family, I can’t do anything about it. This is the new age mafia. There is no one to complain to, no one to argue with, no one to sue. It just... is. ... THIS is the scam of all scams.”10

Tweet by Bruno Skvorc: I just got a reply from @worldlibertyfi . TLDR is, they stole my money, and because it's the @POTUS family, I can't do anything about it. This is the new age mafia. There is no one to complain to, no one to argue with, no one to

![Such functions don’t normally exist in more decentralized cryptocurrencies like bitcoin or ether, but are more common in tokens issued by centralized entities who routinely freeze tokens in sanctioned wallets or that are deemed to be associated with thefts or other illicit activity. Sun defended his actions on September 4, tweeting that he had only “carried out a few general exchange deposit tests” and that “no buying or selling was involved”. He insisted these transfers “could not possibly have any impact on the market” — apparently responding to speculation that he had been selling tokens and thus contributing to WLFI’s price decline, though it remains unclear whether this accusation came from the World Liberty team themselves or from public speculation.6

This move by World Liberty Financial stands in stark contrast to the Trump sons’ frequent complaints about being “debanked” by traditional financial institutions who they say arbitrarily denied them loans and services — the very issue they claimed inspired them to create this project. Sun has publicly appealed to the project team, saying his tokens were “unreasonably frozen” and that he “deserve[s] the same rights” as other early buyers. He wrote, “I call on the team to respect these principles, unlock my tokens, and let’s move forward together toward the success of World Liberty Financials [sic].”7 Perhaps in an attempt to mollify the World Liberty Financial team, Sun tweeted the following day that he planned to purchase](https://media.hachyderm.io/media_attachments/files/115/192/129/882/322/669/original/efe755ee4c9a84e8.png)

Such functions don’t normally exist in more decentralized cryptocurrencies like bitcoin or ether, but are more common in tokens issued by centralized entities who routinely freeze tokens in sanctioned wallets or that are deemed to be associated with thefts or other illicit activity. Sun defended his actions on September 4, tweeting that he had only “carried out a few general exchange deposit tests” and that “no buying or selling was involved”. He insisted these transfers “could not possibly have any impact on the market” — apparently responding to speculation that he had been selling tokens and thus contributing to WLFI’s price decline, though it remains unclear whether this accusation came from the World Liberty team themselves or from public speculation.6

This move by World Liberty Financial stands in stark contrast to the Trump sons’ frequent complaints about being “debanked” by traditional financial institutions who they say arbitrarily denied them loans and services — the very issue they claimed inspired them to create this project. Sun has publicly appealed to the project team, saying his tokens were “unreasonably frozen” and that he “deserve[s] the same rights” as other early buyers. He wrote, “I call on the team to respect these principles, unlock my tokens, and let’s move forward together toward the success of World Liberty Financials [sic].”7 Perhaps in an attempt to mollify the World Liberty Financial team, Sun tweeted the following day that he planned to purchase

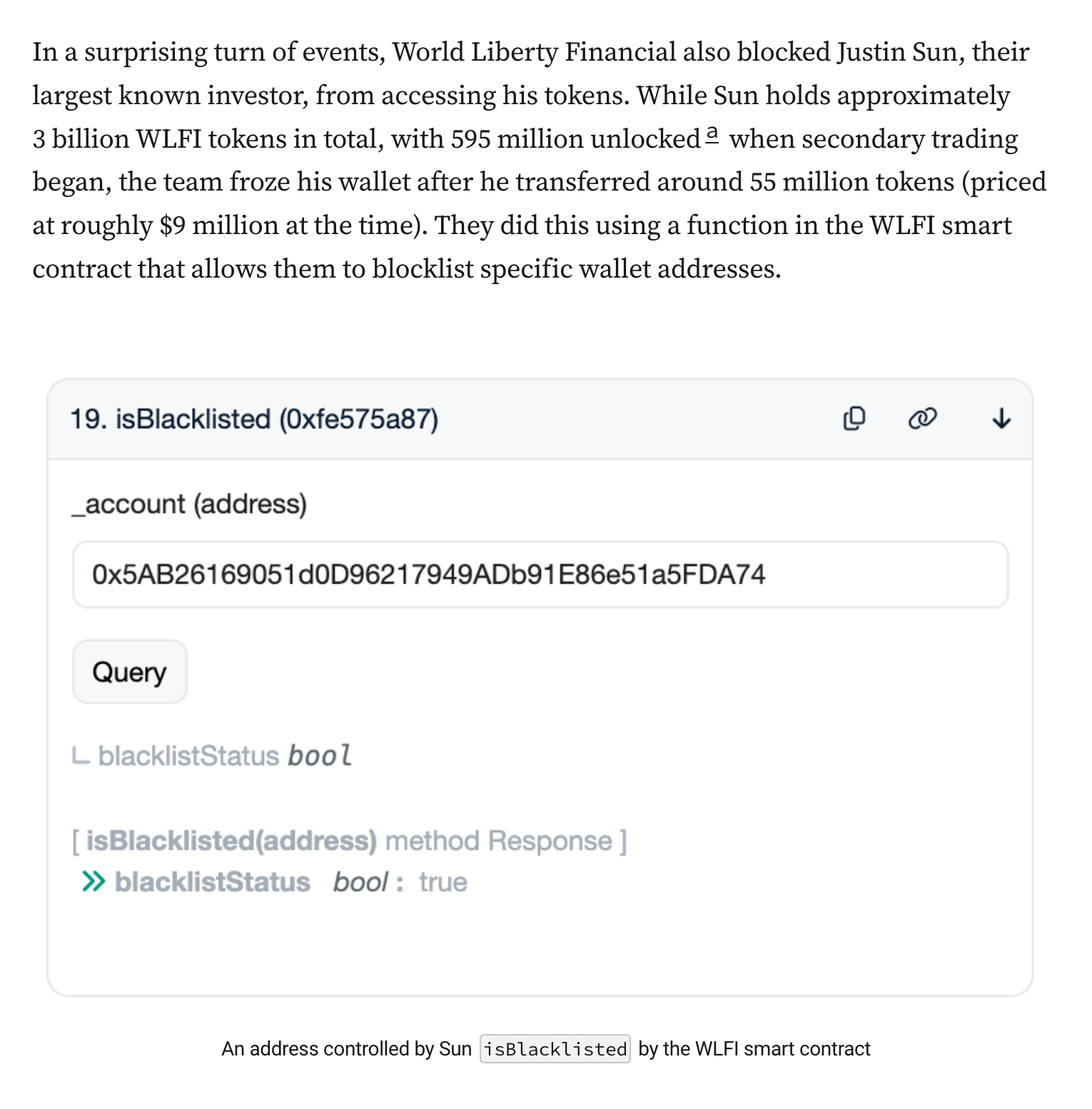

In a surprising turn of events, World Liberty Financial also blocked Justin Sun, their largest known investor, from accessing his tokens. While Sun holds approximately 3 billion WLFI tokens in total, with 595 million unlockeda when secondary trading began, the team froze his wallet after he transferred around 55 million tokens (priced at roughly $9 million at the time). They did this using a function in the WLFI smart contract that allows them to blocklist specific wallet addresses.

Screenshot: A query for isBlacklisted on the wallet 0x5AB26169051d0D96217949ADb91E86e51a5FDA74, showing a response of true

@molly0xfff Wilhoit’s Law. Apparently Justin Sun is part of the out-group today.

@molly0xfff So.... it's going great, then.

@molly0xfff you are only truly liberated from the world's financial monopoly once a grifter denies you your assets. ☝️

@molly0xfff I'm sure we are all very shocked and surprised 😪

The Nasdaq has determined that Eric Trump should not serve on the board of ALT5 Sigma, a treasury company that’s set to buy $750 million WLFI tokens, benefiting him and his family to the tune of $500 million. I guess they have to draw the line somewhere.

![Alt5 Sigma

When I wrote up the news in August that the Trumps and World Liberty Financial were creating a WLFI treasury company with the Nasdaq-listed ALT5 Sigma, I noted [I90]:

[Alt5 Sigma will] add Eric Trump and World Liberty Financial executives Zach Witkoff and Zak Folkman to its board. All three have a financial interest in World Liberty Financial, presenting a blatant conflict of interest in their roles on the ALT5 board.

Evidently, the Nasdaq at least partly agreed, because a new ALT5 Sigma SEC filing has amended their plans to say that “in order to comply with Nasdaq’s listing rules”, Eric Trump will merely be a board observer. Witkoff will still join the board (as chair, no less); Folkman will be an observer and, subject to stockholder approval, a director.11

ALT5 Sigma’s first action as a company will be to purchase $750 million in WLFI tokens to create its treasury. With 75% of WLFI token proceeds going directly to the Trumps, they’ll pocket a cool $500 million, essentially through a deal with themselves.12](https://media.hachyderm.io/media_attachments/files/115/192/142/880/092/042/original/7e90e601000c063f.png)

The Senate published a new discussion draft of their market structure legislation. Senator Warren has issued a statement that the newest proposal “reportedly reflects secret feedback” from the crypto industry that Republicans have refused to share.

![In Congress

Congress has returned from its summer recess, and we will now likely see Republicans pushing hard to pass a crypto market structure bill as quickly as possible. Though the House passed its Clarity Act bill in July [I89], the Senate has so far focused on drafting its own legislation. The Senate Banking Committee published a new draft bill shortly after returning, which, among other things, directs the SEC and CFTC to establish a Joint Advisory Committee on Digital Assets to “further the regulatory harmonization of digital asset policy” between the two agencies. The new bill also includes a new clause regarding tokenized stocks, apparently aimed at addressing concerns (including from me [I88]) that any securities issuer could enjoy a Get Out of SEC Regulation Free card merely by issuing their security on-chain. The new draft states: “any instrument that is a security under the securities laws shall not cease to be a security because that instrument is issued, recorded, represented, or transferred using distributed ledger technology”.13

Banking Committee Ranking Member Elizabeth Warren (D-MA) issued a statement after the draft was released, saying that the newest proposal “reportedly reflects secret feedback from industry and other stakeholders that Republicans refuse to share with Committee Democrats, or the public.” She has slammed the proposals as “industry-written”, and demanded the Republicans release the industry feedback that shaped the bill.14](https://media.hachyderm.io/media_attachments/files/115/192/146/501/871/930/original/d39f5882ee41084a.png)

Pro-crypto Senate Democrats have signaled they’re willing to work on a market structure bill, but have made some demands — including a prohibition on elected officials profiting from crypto projects.

Democrats have made these demands in the past, but typically not the ones who have provided the swing votes for crypto legislation. Now, 11 of 18 Senators who voted for GENIUS have signed on to a letter demanding these changes.

And the letter was authored by Ruben Gallego (D-AZ), who received $10 million from the crypto lobby in 2024. It’s certainly possible that some demands will be dropped during negotiations, but this strikes me as the strongest pushback we’ve seen thus far from pro-crypto Senate Dems.

It’s certainly possible that some demands will be dropped during negotiations, but this strikes me as the strongest pushback we’ve seen thus far from the set of pro-crypto Democrats who’ve in the past provided the votes needed to pass the industry’s favored legislation. The letter was published by Ruben Gallego, one of the two Senate Democrats who received support from the crypto industry super PACs in 2024. Both Gallego and Elissa Slotkin received $10 million in industry backing; Slotkin did not sign on to the framework. (Other Senate Democrats, such as Kirstin Gillibrand, received contributions from individual crypto executives, but were not supported by the PACs. Gillibrand received the most direct support of any Senate Democrats, but at around $100,000 it was considerably less than the PACs contributed.)

![Democrats’ past objections to the Trump family’s crypto self-enrichment, raised during debates over bills like the Genius Act [I84], have yet to seriously threaten the legislation’s passage. However, these objections were raised most loudly by Democrats not likely to support the legislation anyway — not from the same Democratic Senators who provided the necessary votes to pass Genius. This framework was signed by eleven of the eighteen Democrats who voted for the Genius Act, plus Senator Blunt Rochester, who supported Genius during the cloture stage but switched to a no vote on the bill itself. Seven Democratic Senators who voted for Genius did not sign on to this framework: Fetterman (PA), Hassan (NH), Heinrich (NM), Ossoff (GA), Padilla (CA), Rosen (NV), and Slotkin (MI).

Senator State Voted for Genius cloture Voted for Genius Signed framework letter Alsobrooks MD Y Y Y Blunt Rochester DE Y N Y Booker NJ Y Y Y Cortez Masto NV Y Y Y Fetterman PA Y Y N Gallego AZ Y Y Y Gillibrand NY Y Y Y Hassan NH Y Y N Heinrich NM Y Y N Hickenlooper CO N Y Y Kim NJ N Y Y Lujan NM Y Y Y Ossoff GA Y Y N Padilla CA Y Y N Rosen NV Y Y N Schiff CA Y Y Y Slotkin MI Y Y N Warner VA Y Y Y Warnock GA N Y Y](https://media.hachyderm.io/media_attachments/files/115/192/150/588/068/373/original/5f8f241641563842.png)

Democrats’ past objections to the Trump family’s crypto self-enrichment, raised during debates over bills like the Genius Act [I84], have yet to seriously threaten the legislation’s passage. However, these objections were raised most loudly by Democrats not likely to support the legislation anyway — not from the same Democratic Senators who provided the necessary votes to pass Genius. This framework was signed by eleven of the eighteen Democrats who voted for the Genius Act, plus Senator Blunt Rochester, who supported Genius during the cloture stage but switched to a no vote on the bill itself. Seven Democratic Senators who voted for Genius did not sign on to this framework: Fetterman (PA), Hassan (NH), Heinrich (NM), Ossoff (GA), Padilla (CA), Rosen (NV), and Slotkin (MI).

Senator State Voted for Genius cloture Voted for Genius Signed framework letter Alsobrooks MD Y Y Y Blunt Rochester DE Y N Y Booker NJ Y Y Y Cortez Masto NV Y Y Y Fetterman PA Y Y N Gallego AZ Y Y Y Gillibrand NY Y Y Y Hassan NH Y Y N Heinrich NM Y Y N Hickenlooper CO N Y Y Kim NJ N Y Y Lujan NM Y Y Y Ossoff GA Y Y N Padilla CA Y Y N Rosen NV Y Y N Schiff CA Y Y Y Slotkin MI Y Y N Warner VA Y Y Y Warnock GA N Y Y

![The pro-crypto wing of the Senate Democrats has indicated willingness to negotiate a market structure bill, but suggested they will not sign off on one without some conditions. This is both good and bad for the crypto industry: on the one hand, they may get a bill through before the midterm elections, which is priority number one for an industry nervous that the Republican trifecta may not survive past 2026, and wants to see a bill signed into law so that the industry’s “progress” cannot be so easily rolled back. On the other hand, the Democrats are asking for more significant changes than they demanded in negotiations over the Genius Act — some of which could be stumbling blocks if the Democrats stick to their guns.

These include things like amendments to the draft regulation to ensure that the SEC and CFTC have the authority and funding to oversee crypto markets without leaving any assets in a regulatory vacuum, and strengthening consumer protections (including by preserving state regulatory and CFPB authorityb). They also want to see elected officials and their families prohibited from “issuing, endorsing, or profiting from digital assets while in office”, and require disclosures from officials who hold digital assets. They demand that “commissioners from both parties sit at the SEC and CFTC to create a quorum for digital asset rulemakings”, seemingly addressing the concern that Trump will leave the CFTC as a one-man agency [I91].15](https://media.hachyderm.io/media_attachments/files/115/192/150/582/946/415/original/06643bf77b70793b.png)

The pro-crypto wing of the Senate Democrats has indicated willingness to negotiate a market structure bill, but suggested they will not sign off on one without some conditions. This is both good and bad for the crypto industry: on the one hand, they may get a bill through before the midterm elections, which is priority number one for an industry nervous that the Republican trifecta may not survive past 2026, and wants to see a bill signed into law so that the industry’s “progress” cannot be so easily rolled back. On the other hand, the Democrats are asking for more significant changes than they demanded in negotiations over the Genius Act — some of which could be stumbling blocks if the Democrats stick to their guns.

These include things like amendments to the draft regulation to ensure that the SEC and CFTC have the authority and funding to oversee crypto markets without leaving any assets in a regulatory vacuum, and strengthening consumer protections (including by preserving state regulatory and CFPB authorityb). They also want to see elected officials and their families prohibited from “issuing, endorsing, or profiting from digital assets while in office”, and require disclosures from officials who hold digital assets. They demand that “commissioners from both parties sit at the SEC and CFTC to create a quorum for digital asset rulemakings”, seemingly addressing the concern that Trump will leave the CFTC as a one-man agency [I91].15

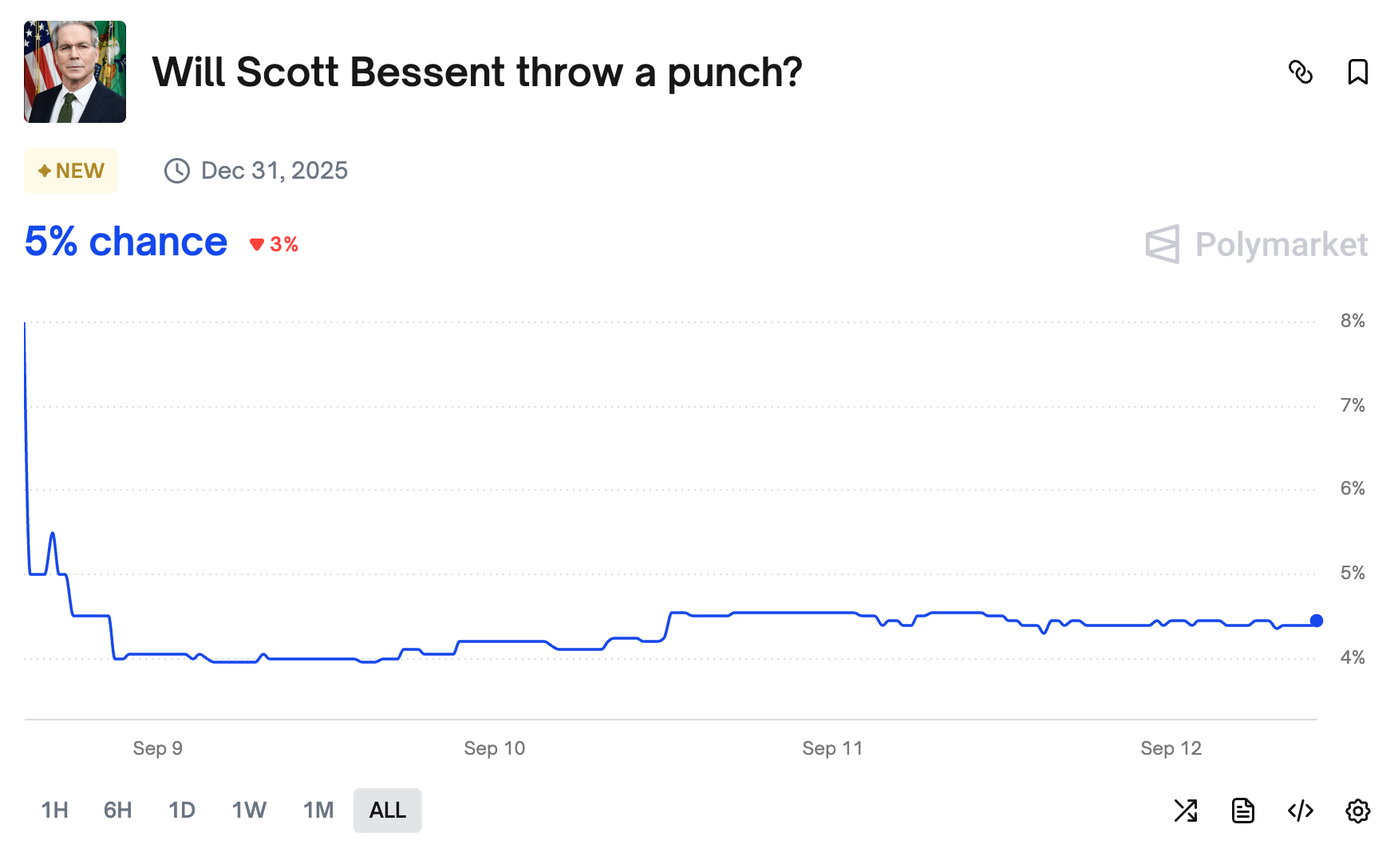

The CFTC has issued a no-action letter greenlighting Polymarket to start opening up to US customers. Thank goodness: in the future, when Treasury Sec Scott Bessent threatens to punch FHFA director Bill Pulte in the face, US speculators will be able to gamble on the likelihood that Bessent actually throws a punch.

Prediction market for “Will Scott Bessent throw a punch?” “Yes” began at around 8%, quickly dropping to hover between 4-5%.

![In regulators

The CFTC has issued a no-action letter with respect to QCX, the tiny derivatives exchange Polymarket acquired in July to get their hands on its Designated Contract Markets (DCM) license [I89].16 This essentially gives Polymarket the okay to begin offering their prediction markets in the US — though given how many Americans already trade on the platform despite its supposed prohibitions, more than a few people were surprised to learn they even needed such approval. Prediction markets were once a rare phenomenon in the US — or strictly limited academic exercises — thanks to CFTC oversight that prohibited platforms from offering the types of sports, elections, and current events contracts that are now popular. Now even the academic exercise (a non-profit platform called PredictIt) will be expanding its US operations with a recent okay from the CFTC.17

Heavy pressure from these platforms in and outside of court, a favorable court ruling [I66], and new CFTC leadership that thinks these platforms are “an important new frontier”18 has resulted in this explosion of places where people can bet (sorry, trade) on everything from who will win an election or sports game, to what words public officials will use in speeches, to which countries will airstrike one another. Now when Treasury Secretary Scott Bessent threatens to punch Federal Housing Finance Agency director Bill Pulte in the face,19 speculators can gamble on the likelihood that Bessent actually throws a punch (tr](https://media.hachyderm.io/media_attachments/files/115/192/170/600/006/934/original/8728d7362e5a6ded.png)

In regulators

The CFTC has issued a no-action letter with respect to QCX, the tiny derivatives exchange Polymarket acquired in July to get their hands on its Designated Contract Markets (DCM) license [I89].16 This essentially gives Polymarket the okay to begin offering their prediction markets in the US — though given how many Americans already trade on the platform despite its supposed prohibitions, more than a few people were surprised to learn they even needed such approval. Prediction markets were once a rare phenomenon in the US — or strictly limited academic exercises — thanks to CFTC oversight that prohibited platforms from offering the types of sports, elections, and current events contracts that are now popular. Now even the academic exercise (a non-profit platform called PredictIt) will be expanding its US operations with a recent okay from the CFTC.17

Heavy pressure from these platforms in and outside of court, a favorable court ruling [I66], and new CFTC leadership that thinks these platforms are “an important new frontier”18 has resulted in this explosion of places where people can bet (sorry, trade) on everything from who will win an election or sports game, to what words public officials will use in speeches, to which countries will airstrike one another. Now when Treasury Secretary Scott Bessent threatens to punch Federal Housing Finance Agency director Bill Pulte in the face,19 speculators can gamble on the likelihood that Bessent actually throws a punch (tr

1+ more replies (not shown)

bonfire.cafe

A space for Bonfire maintainers and contributors to communicate

Automatic federation enabled