@cdonat literally zero people use that. Anything which requires installing yet another app is a non-starter.

Post

Replies:

0

@janikvonrotz I'm sure it'll be ready just as soon as GNU Hurd is 😆

@Edent Good things take time 😉

But seriously, I hate paying online no matter the provider. They all suck.

I hope for a european, instant, inter-banking payment system / standard / protocol.

@janikvonrotz @Edent GNU Taler is here - I already did some donations with it.

@itsFriday @Edent More details! How did you add talers with your bank?

@janikvonrotz @Edent It is possible with https://taler-ops.ch and a swiss bank account. It has some rough edges but works fine.

Here is a good article (in German) for an easy start: https://gnulinux.ch/gnu-taler-mit-echtgeld-ausprobiert-teil-1

@itsFriday thanks! The website says it is "immune to chargeback fraud". Does that mean if I pay with Taler and the merchant doesn't deliver, I cannot do a chargeback?

@Edent As I understand it, yes. It is like with cash.

@itsFriday ah, that's a shame.

It also looks like the merchant gets no info about the customer - which might also be problematic if an individual/company is sanctioned.sanctioned

I'm sure it is a technically clever system, but doesn't seem to meet user needs.

@Edent Sure it may not fit all cases. I think it would however match exactly for this usecase here to donate to toots. The author gets money and can proof how much and the donor does not need to share personal data.

Needing to sign up to a system and then not knowing what data is shared or even are required to share is a hughe blocker for me to donate.

@itsFriday yes, but if I receive money from a sanctioned individual or as the proceeds of a crime, it isn't going to end well for me.

@Edent If the system works as intended, no one knows who sent money to you.

But the excange knows who sends the money to them and they can and should block such money from being convertet into Taler in the first place.

Am not sure what the excange can do about money already as Taler when some one get sanctioned. Since they now the recipient, they should at least be able to block sanctioned people from receiveing more money.

@itsFriday so if someone steals a bunch of money and converts it to Taler, they can send it to someone else?

Sounds an awful lot like it would be useful for money laundering.

@Edent I don't know the details, but there are regulations in place - maybe more than with cash. And you don't need to accept an incoming transaction if it is suspicious like unusually high.

@Edent

The technical side of microtransactions is simple - anyone can add a button wherever. Getting a payment processor to perform the actual financial transaction has so far been more or less impossible.

The only payment processor that any fraction of people actually use are Visa/MasterCard - and they will change you ~30¢ + %5 per transaction, so you will lose money (be charged more than the tip is worth) on every tip you are sent that's under ~$1.

@duncanlock I don't know where you are in the world, but in the UK and Europe it is free to transfer a single penny to any account.

I use tap-to-pay on low value transactions all the time. I even bought a single apple from a greengrocer once!

@Edent @duncanlock Pretty sure there would be a merchant fee and the shop just ate it

@davidgerard @Edent @duncanlock Yes, the shop will have paid the transaction fee for this and it will have been a fairly large proportion of the payment.

Not as large in the UK as in the USA, but still a flat fee per transaction plus a percentage of the payment amount.

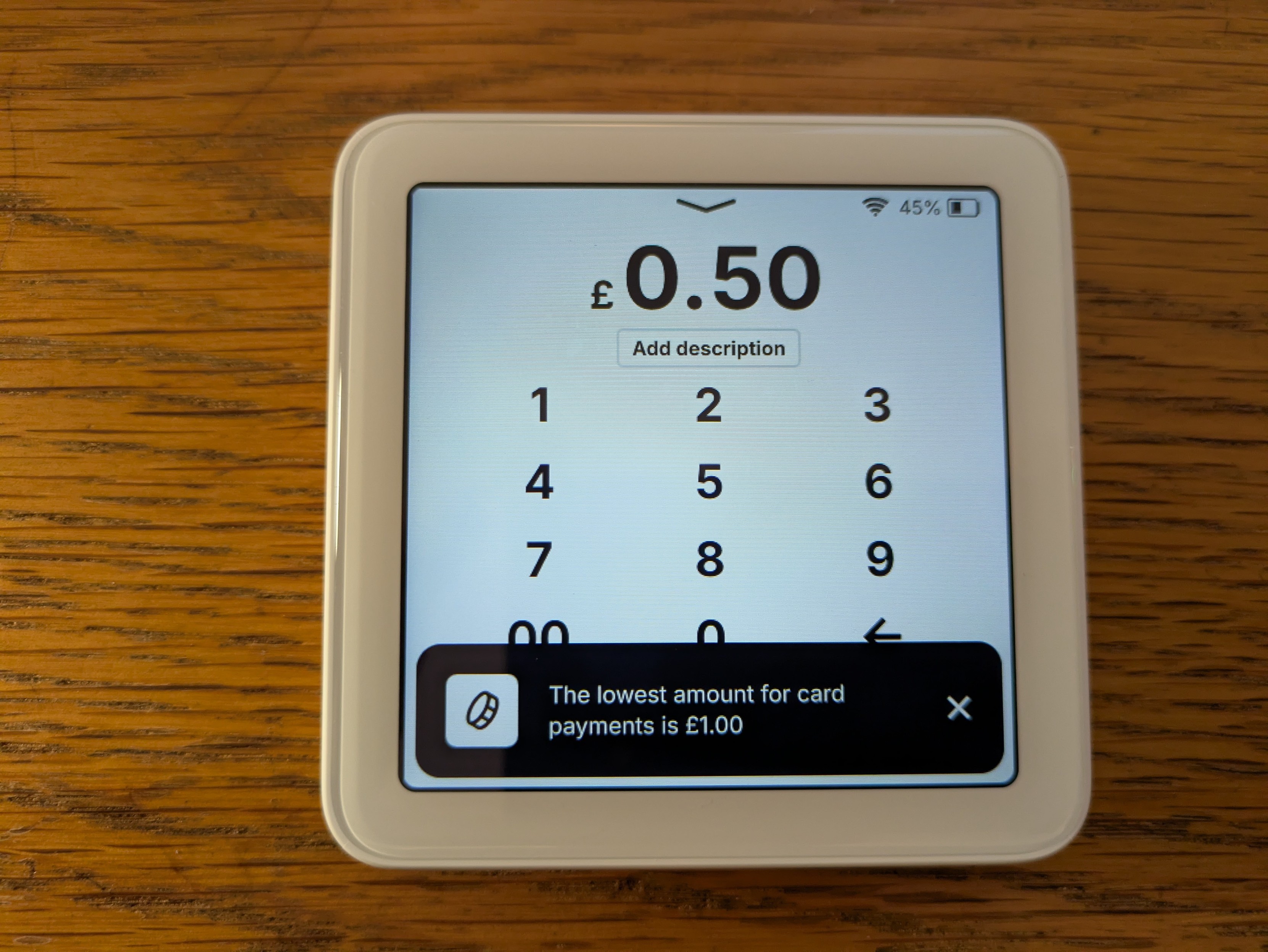

The payment providers that offer simple percentage pricing (eg. Square at 1.75% and SumUp at 1.69%) are able to do so because they insist on a minimum transaction amount of £1.

@steve @Edent @duncanlock yeah, lotta corner shops round here still say minimum £5. Even the ones that don't, i keep coins in my pocket so i can buy a drink or whatever without their share being eaten in card fees.

@davidgerard @Edent @duncanlock yes. Using cards (even non-credit cards) costs the seller money.

@davidgerard @duncanlock @tante

Not really. In the UK, I pay a fixed % for tap-to-pay card transactions.

SumUp charge as little as 0.99% whether you're charging £1 or £500. My corner shop prefers that I pay by card for a chocolate bar rather than a £20 note.

@Edent @davidgerard @duncanlock @tante SumUp's minimum payment amount in the UK is £1.

Their fees are rounded to a whole number of pennies per transaction using Banker's rounding (Round Half to Even).

@davidgerard @duncanlock @tante @steve ah, I misread their developer documentation.

I don't know which merchant my greengrocer uses, but they're able to charge less than a quid.

Of course, that's card-present. Looks like online payments still have a fixed fee overhead.

Thanks!

@Edent The "traditional" card terminal providers like Barclaycard, Dojo, Worldpay and so on will have fee structures that incorporate a fixed "authorisation fee" and then a percentage of the payment which are likely to be different for each class of card (matrix of credit, debit, domestic, international, special case for Amex); they will happily process transactions that cost the merchant more than the transaction amount. They tend to pay out gross daily and then invoice fees monthly.

@Edent think it would be great to something like this. Lots of creatives I'd like the option to easily tip. Could it be done in a client app?